The Loan-to-Value (LTV) ratio is a critical measurement used by financial institutions during the mortgage underwriting process. This ratio serves as a tool for lenders to evaluate the risk associated with lending money to potential homeowners. Gaining a comprehensive understanding of the LTV ratio is essential for anyone aiming to make informed decisions regarding their financial future, particularly those involving home buying or refinancing processes.

The LTV ratio is a straightforward yet essential calculation in the mortgage industry. It compares the size of a loan you are seeking against the appraised value of the property you intend to purchase or refinance. Expressed as a percentage, the LTV ratio is a determinant of loan risk for lenders. Essentially, a lower LTV ratio signifies reduced risk from a lender’s viewpoint, whereas a higher LTV ratio is associated with an increased amount of risk, making the lending situation less favorable for the lender.

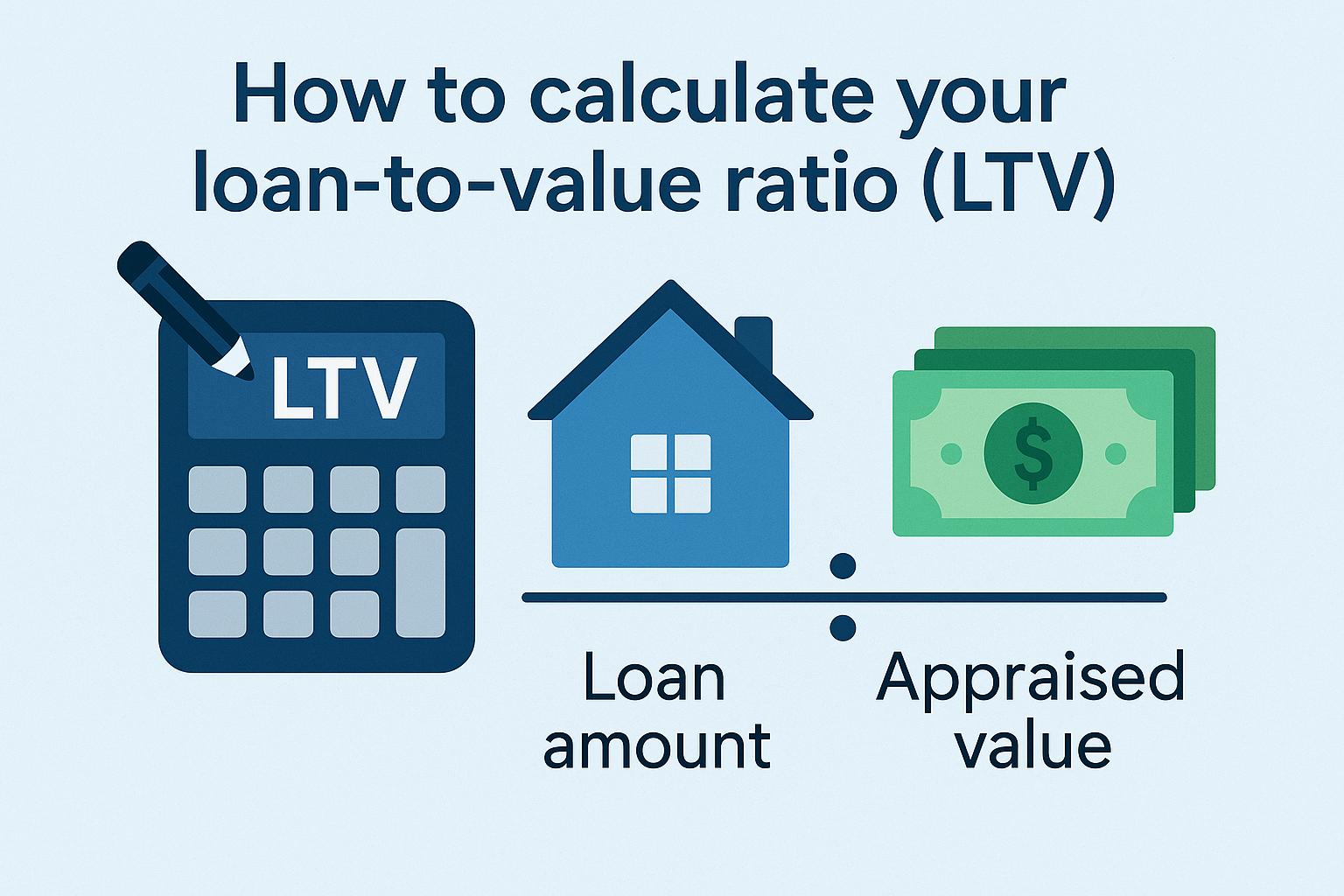

Calculating your LTV ratio is a matter of understanding some basic arithmetic and having the necessary information at hand. Here’s how you can calculate it:

The first step in calculating your LTV ratio involves determining the total loan amount. This amount represents the sum you are either borrowing to purchase a home or the remaining balance if you are considering refinancing an existing loan. Essentially, the loan amount serves as the numerator in your LTV calculation.

Acquiring the appraised value of the property is your next task. This appraised value refers to the property’s current market value, which is usually determined by a qualified, professional appraiser. The appraisal provides a realistic estimate of the property’s worth and is critical as it anchors your calculation, acting as the denominator in the LTV formula.

With the necessary information in hand, proceed to calculate the LTV ratio. This process involves dividing the loan amount by the appraised property value, then converting it to a percentage by multiplying by 100. The formula for the LTV ratio is as follows:

LTV Ratio (%) = (Loan Amount / Appraised Property Value) x 100

Example: Consider a scenario where you are borrowing $200,000 for a property that has an appraised value of $250,000. Your calculation would look like this:

LTV Ratio = ($200,000 / $250,000) x 100 = 80%

The significance of the LTV ratio is multi-faceted in the mortgage realm. Lenders assign considerable weight to this ratio when making decisions about loan approvals and determining the terms associated with a loan. A reduced LTV ratio typically results in more favorable interest rates and loan conditions since the lender perceives less risk. Conversely, a higher LTV ratio can signal increased risk, which may lead to higher interest rates or make it more challenging to obtain financing.

The LTV ratio also affects the requirement for private mortgage insurance (PMI). Lenders often stipulate that if your LTV ratio exceeds a certain threshold, generally 80%, you are required to carry PMI. This insurance serves to protect the lender in the event of default. However, while PMI provides protection for lenders, it also results in additional costs for the borrower, thus increasing the total expense of obtaining a loan.

Understanding the nuances of LTV ratios extends beyond just mortgage terms and risk assessment. Various types of refinancing, home equity lines of credit, and other financial products also rely on LTV ratios to determine eligibility and terms. Additionally, regional property market conditions can impact appraisals, which influence LTV calculations indirectly.

Market volatility further adds a layer of complexity to the LTV ratio. In rapidly changing markets, the appraised value of a property might vary considerably over short periods. These shifts can influence the initial calculation of an LTV ratio, thus impacting refinancing options or new borrowing scenarios. Understanding how to navigate these market conditions can be crucial for making informed loan decisions.

In closing, having a solid grasp of the Loan-to-Value ratio is invaluable for anyone engaged in the process of acquiring or refinancing a home. This ratio plays a pivotal role in the assessment of loan risk, setting interest rates, and requiring mortgage insurance. As such, calculating your LTV provides critical insights into your financial standing regarding your property and future borrowing potential. For more detailed information on different mortgage calculations and strategies, consider consulting financial advisors or [trusted financial websites](#). Exploring these sources can unlock further understanding of home financing and valuable resources when making significant financial decisions.

This article was last updated on: May 3, 2026