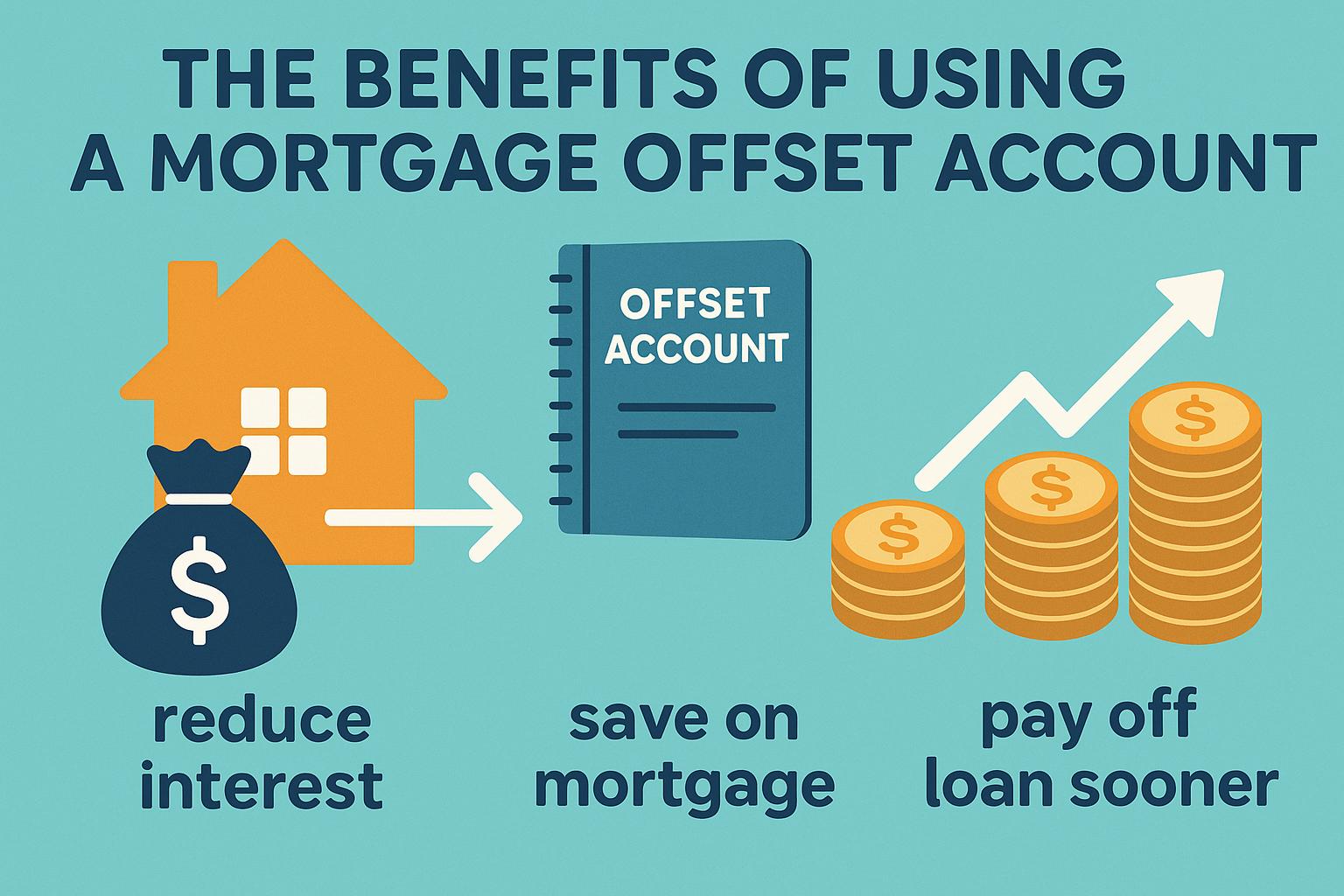

A mortgage offset account serves as a transaction account that is directly linked to your mortgage. The principal function of this account is to offset the balance against your outstanding loan. Essentially, rather than earning interest on the savings deposited in this account, you are effectively reducing the interest that applies to your mortgage. Utilizing this feature can lead to a substantial decrease in the overall interest that you would otherwise be required to pay over the duration of your mortgage. As a result, this mechanism has the added benefit of potentially accelerating your loan repayment schedule.

The operation of a mortgage offset account is relatively straightforward. The balance held within this offset account is subtracted from the remaining balance of your mortgage when the interest is calculated. For example, if you have an outstanding mortgage amounting to $300,000 and you maintain a balance of $20,000 in your offset account, interest would only be calculated on $280,000 of the mortgage. This leads to less interest being charged overall, reflecting a direct and immediately observable benefit.

Saving on Interest: One of the key financial advantages of utilizing a mortgage offset account is the ability to save considerably on interest payments. By effectively reducing the portion of the mortgage balance that is subject to interest calculations, you stand to pay significantly less in interest charges over time. This advantage becomes particularly evident over the life of a long-term mortgage, where cumulative interest payments can be substantial.

Shortening the Loan Term: Another noteworthy benefit is the potential reduction in the loan’s term. By decreasing the amount of interest accrued, a larger proportion of each regular repayment contributes directly to diminishing the principal balance. Consequently, this process can lead to a shorter loan term, allowing you to pay off your mortgage earlier than initially planned.

A mortgage offset account is distinguished by the financial flexibility it offers to users. Unlike making additional repayments directly toward your mortgage—where accessibility to those funds may be limited—an offset account often allows for more accessible management of funds. You can generally withdraw or transfer money from your offset account relatively easily, which can prove advantageous when managing unexpected expenses or during financial emergencies.

Before deciding to integrate an offset account with your mortgage, it is critical to weigh some important considerations. First, it should be noted that these accounts might incur additional fees or charges. Furthermore, there is often a potential requirement for a higher interest rate when compared to non-offset mortgage products. Consequently, maintaining a higher balance within the offset account is more beneficial and possibly necessary to reap its advantages effectively. Due to these stipulations, offset accounts may not be suitable for every borrower, especially those who might find it challenging to maintain a consistently high balance.

For individuals seeking more comprehensive insights into the workings of mortgage offset accounts, it would be prudent to engage with financial advisors or refer to resources available through reputable financial institutions that provide in-depth mortgage services.

This article was last updated on: March 8, 2026